Proposed SEC disclosure rule a disaster

Proposed SEC disclosure rule a disaster

The Great Shrug must continue.

On Monday, the SEC followed through with it’s threat promise to require public companies to report their greenhouse gas emissions, as well as provide details on how climate change is effecting their business. Said SEC Chairman Gary Gensler:

Our core bargain from the 1930s is that investors get to decide which risks to take, as long as public companies provide full and fair disclosure and are truthful in those disclosures. That principle applies equally to our environmental-related disclosures.

The challenge, like with all regulations meant to push a political narrative, is what to do when it comes to reporting on Scope 3 emissions. Scope 3 emissions are those created by customers downstream of the sales point. For oil and gas companies, that means powering transportation, generating electricity and heating homes and having O&G account for it. Can you imagine if the SEC required “sugar reporting” and made McDonald’s and Coca Cola responsible for the downstream caloric consumption? It wouldn’t take much imagination to foresee the lawsuits that would come from all the obese people, hospitals and insurance companies looking to displace the financial burden for their own eating choices. Welcome to the world devoid of personal responsibility. Jump into my nightmare, the water is warm.

Back to reality, for emissions, the SEC says it would put the onus on companies to determine whether their Scope 3 emissions are "material.” According to IHS Markit, 88% of emissions from the oil and gas sector are scope 3 which makes defining “material” challenging. But, by adding significant specificity to financial reporting on climate change and proposing candidates like Saule Omarova for the Federal Reserve Board who say that:

A lot of the smaller players in that industry are going to, probably, go bankrupt in short order — at least, we want them to go bankrupt if we want to tackle climate change.

As always, what lacks in the conversation is the recognition that it is consumers who make the choice to consume, that prices are based on traders who decide whether to buy or sell the commodity based on the supply demand paradigm and oil and gas companies simply produce it and see what happens. As we pointed out in our “Windfall Taxes: A Rebuttal” piece for Ms. Warren, in 2021 the top four E&Ps produced a paltry 7.5% return on P,P&E which holds a trillion dollar balance. Companies are entirely beholden to the rock they acquired and the prevailing commodity price at the time they drill, and yet they remain the villains of humanity. From windfall profits to carbon taxes for “the social cost of carbon,” disassociation from consumption reigns supreme.

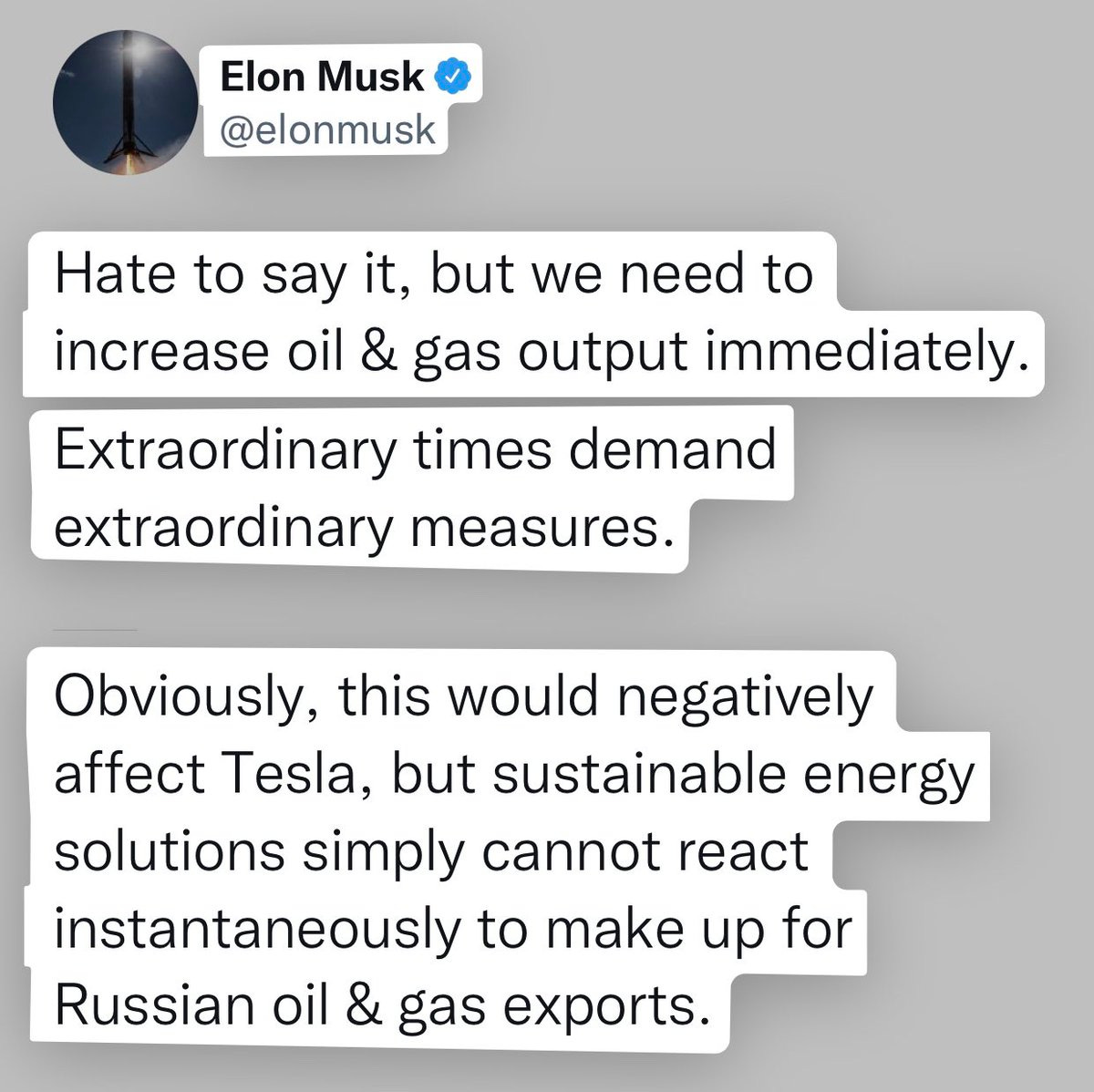

For the SEC, even if one ignores the questions “How can they be taken seriously when Elon Musk constantly trolls them and under their purview, SPACs, MLPs and every other manner of financial tom foolery has been perpetrated?”, one must ask “What is the point of being public if you are an oil and gas company?”

The answer, increasingly, is “There is no point.” And thus, the great shrug must continue to maximize the value to shareholders until rational energy policy returns to Washington, D.C. What does that look like?

Pay down as much debt as possible so the activist banks can’t kick your legs out from under you and refuse to finance you at your weakest.

Hedge to lock in returns and buy back as many shares as possible with the free cash flow assuming that it is an accretive PV transaction.

Continue to consolidate into a very small number of very large companies with huge cash flow and the power to manage ESG and public pressure in the interim.

Ultimately, consider delisting from the US and European markets, either by going private and circumventing SEC reporting or list in a country that doesn’t require climate reporting.

Ironically, the less oil and gas produced by private and national oil companies from hostile regimes, the higher the prices go, which makes for an interesting perverse incentive with no ability to publicly put pressure on these companies. Larry Fink understands this dilemma well.

Speaking at the Green Horizon Summit chaired by CNBC’s Julianna Tatelbaum during the COP26 climate conference in Glasgow, Scotland, Fink praised public companies for increasing their reporting of emissions but criticized oil firms for selling parts of their businesses to private investors, and said it could create huge market arbitrage.

“We can’t just ask public companies to move forward without the rest of society. It’s going to create the biggest capital market arbitrage. We’re seeing that more hydrocarbons have been sold to private companies in the last few years than almost any time ever. That doesn’t change the world at all. It actually makes it, the world even worse, because it moves from public disclosed companies to opaque private enterprises. So, the mission is failing if that’s all you’re doing,” he stated.

It is therefore not insignificant that Warren Buffet has been buying Oxy stock of late. And lots of it. Berkshire Hathaway now owns 136 million shares, representing 13% of the company with another 84 million warrants at $59.62, which if exercised, would raise Oxy another $5 billion in cash and increase his stake to nearly 20%. Berkshire also holds $10 billion worth of preferred debt, paying 8%. Buffet may not live forever, but clearly Berkshire Hathaway only cares about making money for it’s shareholders and, having never split their stock, they do what’s right, not what sounds good in a press release.

A private Oxy would have a tremendous amount of flexibility to pursue it’s low carbon business plan, not because it’s “green washed” for public consumption but because it actually makes them lots of money. It would also allow them to expand their international footprint as Tier 1 inventory in the United States continues to deplete rapidly.

Which is why it makes me wonder when Elon Musk may deploy some of his $245 billion of personal wealth to privatize “a Conoco” and sell Tesla’s through their expansive service station network.

It would seem to me, the only person who cares less about what people think than Warren Buffet is Elon Musk. And he just wants to make money and keep trolling the SEC.

I hope BOD's of O and G companies are hankering from some tough love from Director DRW. If not, they will flail and fail, and deservedly so. Characteristically incisive AND entertaining...no small feat.