Bump… set … silence

Bump… set … silence

The majors and API defer advocacy in the face of blatant misinformation

In today’s post, we have a two-fer, as we dive into a great piece on CNBC from Brian Sullivan and a discussion on the evolving landscape for private E&Ps from Doug Sheridan on LinkedIn.

I got to know Brian Sullivan in the lead up to being invited onto CNBC’s “Fast Money” March 18, 2020, where I was invited to come on the show and talk about the disaster that was coming. I got the invite the day before the show, as it happens with media appearances, and I had a conflict with a very important game of banker. No problem, I thought. I’d quit at 14 and take the call from the clubhouse. It was, after all, only a 3 minute segment and it seemed like a waste to give up an afternoon when it wasn’t clear if the world was ending later that week or not. Sports arenas were half full. Restaurants were dead. To be downtown felt like you were in “I am Legend,” and I wasn’t sure if I was the living person, the zoo animals or the zombies. Then the unbelievable happened and California did in fact issue a state wide “stay at home” order the next day that led to a cascade of closures around the U.S, and what we now affectionately know as “the last 14 days.”

As it happened, I was up all the money in banker and being the competitive person I am, I wanted to have my cake and to eat it, too. What goes better with an appearance on CNBC? Winning money golfing while doing it! As if the golf gods had willed it to be so, the call was timed in the perfect place. I sprinted from the 14th green into an office building off the 15th hole, pulled open the door and took the call from a vacant conference room in a building in which I didn’t work. I finished the segment and made it back in time to hit my tee shot. I hit a beauty right at the pin. “You like apples? How do you like them apples… Press!!”

During the segment, I said with everything going on with the lockdowns, oil was going to $0/bbl (I was wrong.. it went to -$37/bbl) and Brian responded “Well, it’s a good thing you sold you company, then.” With that kind of honesty, you know we were destined to become friends.

To this day, we chat about once a month and I have always loved his pragmatism. At all stages of the pandemic, the energy price gyrations and back to the financial crisis of 2008, he is consistent, logical and doesn’t promote the narrative du jour. And I give him huge kudos. When a doctor friend in early 2020 told him obesity was a contributing factor to negative outcomes for COVID, he took it upon himself to lose 30 lbs. Personal responsibility for the win.

Flash forward to oil today, what a difference 24 months makes! As I assess the landscape in 2022 and looking at OneEnergy’s “sister Permian companies” who started their adventure at the same time as we started ours, companies such as Colgate, Tap Rock and Ameredev, with 2 “4-ish billion” IPO’s being evaluated, hindsight is literally 2020.

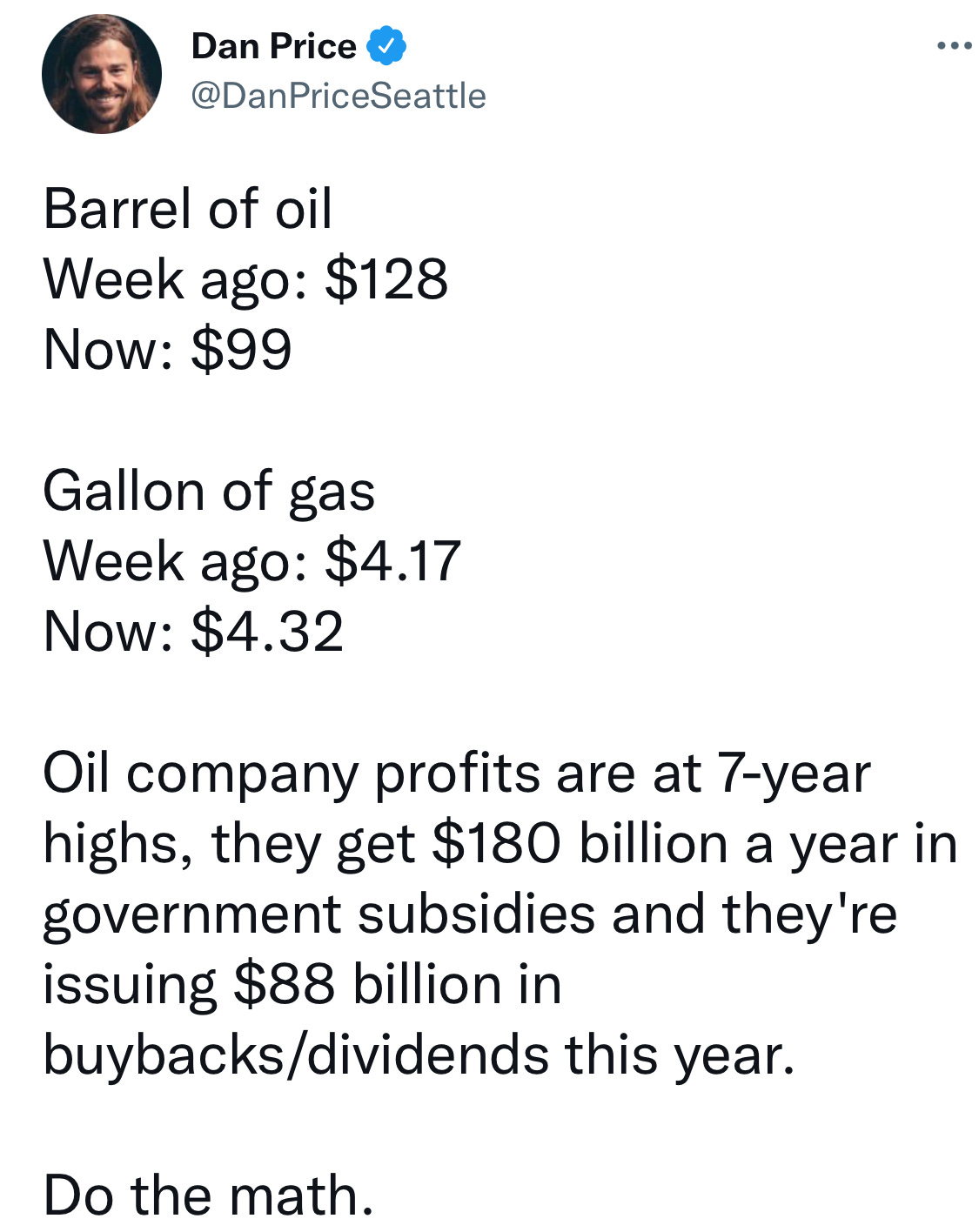

The headwind to oil and gas now? Inventory, capital and hatred, the latter of which is clear as the rabble-rousing continues from the usual case of characters: Bernie, Liz and super socialist Dan Price, who cherry pick data to fire up an uneducated base, ignoring entirely the principles of supply-demand and timing….

Enter Brian Sullivan March 17, 2022. His family used to own gas stations and he knows the industry well, having covered it for almost two decades. He sees a narrative being spun on the ”gasoline prices” topic so he took it head on. “Why are gasoline prices not perfectly correlated to oil prices? Well, I’ll tell you….”

Using his usual pragmatic approach, he strikes at the heart of the issue in this 3 minute segment. I encourage you to share it to your network.

Well done, Brian. Thank you on behalf of industry.

While we are on the subject of Private E&Ps, I turn to a Doug Sheridan post on LinkedIn.

As one thinks about the changing landscape of U.S. oil and gas producers, PE companies such as Ameredev, Tap Rock and Colgate (and I’ll include the OneEnergy acquirer Franklin Mountain in this group) are able to “drill their returns” and work off a low production base with relatively low hedges to aggressively develop their assets at what have turned out to be exceptional single well economics, with rates of returns far in excess of 100%. Between those 4 companies alone, they are running over 20 rigs and have the ability to significantly outspend cash flow and grow production if they do choose.

Felix and Double Point set the template for PE companies to ramp up and they both successfully excited in difficult environments, selling to WPX (now Devon, who is rumored to have made a $6 billion offer for Exxon’s Bakken assets, according to Reuters) and Pioneer. The ramp in production and cash flow made the cash flow metrics “reasonable” and enabled the buyers to sell it to their investors. Many PE firms have tried to follow that model since.

But equally impressive, before ramping up was cool, Birch Resources has quietly drilled with 5 rigs on 18,000 acres since 2018/2019 to fully develop 100% of their acreage and turn “potential” into production. 2020 was a hiccup but I was always impressed by that team’s conviction, foresight and execution.

Bottom line, as the “acquire and flip” model came to an end in 2018, “drill your returns” is the best way to take PV30 locations and turn them into PV10 production, which after payout of your capital, makes the “sale of the tail” simply a call on macro price, much of which can be hedged away since the spread from PV30-PV10 was already captured. The challenge here remains that publics want that spread, too, and may not want to buy the tail. Time will tell,

But moving past PE companies brings you to the mega Privates. Hilcorp in Alaska et al and in the Permian you meet Endeavor and Mewbourne, long standing private, family run oil businesses. Here, I turn it over to Doug.

The WSJ writes, with oil prices gyrating around $100 a barrel, Autry Stephens’s company, Endeavor Energy Resources, LP, and a few other privately held US drillers, have emerged as pivotal players in the global energy market. It's making them a lot of money.

Stephens, who turned 84 last week, may be the biggest winner. He now has become one of the wealthiest people in the American energy sector, with a reported net worth of more than $10 billion.

It wasn't a given. In April 2020, the pandemic triggered such a sharp drop in oil demand, and oil prices briefly dipped below zero. By that summer, though, with oil prices above $40 a barrel, Endeavor was drilling new wells in the Spraberry, becoming one of the first companies to slowly step up production. Since then, things have only gotten better.

Meanwhile, publicly traded E&Ps, as well as those controlled by private-equity firms, have been cautious about ramping up drilling. Pressure from investors who prefer dividends and share buybacks to ambitious and expensive drilling plans is a big reason. The push to reduce emissions has also curbed their appetite to drill.

But Stephens feels few such pressures. Neither do a few other family-controlled drillers, including Mewbourne Oil Co, owned by 86-year-old Curtis Mewbourne. Over the years, these companies have rebuffed suitors, borrowed money from banks and others and relied on their own cash to fuel their drilling, giving them freer rein to search for new wells than those who answer to outside shareholders.

It's a particularly powerful formula for today's landscape. Stephens says he has never before seen a market with surging prices yet so little competition. “This is almost too good to be true,” he said.

Together, Endeavor and Mewbourne currently operate 33 oil-and-gas drilling rigs in the US, according to Pickering Energy Partners, up from five in 2020. By comparison, ExxonMobil and Chevron operate a combined 27 drilling rigs in the US, down from 33 in 2020.

By the end of this year, Endeavor and Mewbourne will together produce about 433,000 bpd, or 4% of the US production. The two companies will add 116,000 barrels a day this year, or 18% of the nation’s anticipated production growth.

To Sum It Up: Today, 62% of the 734 active US oil-and-gas rigs are operated by private companies like Endeavor, compared with 49% of the 1,106 rigs at the start of 2019, according to Enverus. The growth isn't over yet.

Our Take 1: It's good to see a few companies be rewarded for bucking the discipline dogma that's gripped the sector. Their initiative and willingness to take calculated risks makes the industry more attractive, not less.

Our Take 2: While most public E&Ps could never have been so nimble or opportunistic as Endeavor or Melbourne, it does make one wonder what could have been if they'd just been a bit more open to challenging the conventional wisdom that's dictated their strategies.

Mr. Stephens and Mr. Mewbourne are legends. They have been through it all, multiple times and their companies are rare in the American corporate landscape. Their positions could never be replicated. In an industry deep into the consolidation phase, the open question to be answered in the years to come is “do private’s have such a structural advantage over public’s with ESG pressures that access to public capital becomes too much of a pain in the a$$ and the industry doubles down on “Midland style?” Time will tell but in the meantime, you have to tip your hat to their conviction.