Kimmeridge and SilverBow

Can’t we all just get along??

Over the past month or so, the industry has seen a small battle emerge in “The Consolidation Games.” They are like “the Hunger Games” but instead of death and such, they are over executive compensation, options and ego, the last of which usually playing an outsized role. But it’s a great saga and worth spending some time on.

What’s happening?

Kimmeridge, a well respected Private Equity firm who’s wins/activism have included the Ares sale to PDC, an Ovintiv activist campaign and quite a successful reconditioning of the DJ Basin under Civitas and having brought in Chris Doyle et al to oversee that company’s transformation, is back at is. In their most recent act, they would see their private portfolio company, Kimmeridge Gas Texas, LLC (KGT) merge with SilverBow. More on Kimmeridge later.

SilverBow for it’s part, is the former Swift Energy Company, and back in my 2013-2015 Eagleford days before OneEnergy, I had spent a lot of time understanding this company and trying to figure out ways to merge with it as well. Bigger was better. Even in 2014, but I obviously never figured out a way to get it done.

Today, SilverBow is much different than it was then, but the core assets remain and as I’ve said for the better part of 6 years, there are too many CEOs per BOE, consolidation is a must and at some point we end up with 10 massive public companies and 10 relevant private companies like Hilcorp to take the US oil and gas industry into the next phase. So like many of their peers, they will be involved in the Consolidation Games eventually. The truth is the future of oil is international and declining inventory, especially in basins like the Eagleford make these plumbing projects commodity price plays through assets not upside. There really should only be a handful of operators in every basin but the Permian and the Eagleford needs to play musical chairs in a big way.

As I look at the proposed transaction…. (Disclaimer: don’t get mad at me, this isn’t investment advice blah blah blah… CDEV really didn’t appreciate my commentary in 2019 but what - is someone going to fire me? Can’t! I’m retired!) I actually agree with the SilverBow board on this one. This isn’t a good deal for SilverBow. I don’t own shares, I won’t buy shares anytime soon, my views only etc etc. But I wouldn’t vote to approve the deal. My reasons they should reject the deal are three fold.

The SMOG values between the two companies are nowhere close and it’s clear Kimmeridge is being opportunistic, aggressive, and loud. All traits I very much admire. But still, SBOW can’t take this deal. To me, it’s dilutive to asset value and “best in class governance” isn’t a value proposition - it should be a baseline.

The KGT assets are much deeper into the gas window. So yes, operating costs are lower but a lot of their development areas look … well… very early in their development and while the SEC deck is run at $2.64/mmbtu gas prices are sub $2/ and at that price, cash flow is substantially risked as are development economics. It is the true challenge of natural gas assets. If you aren’t Marcellus, you are marginal.

KGT recently bolted on a private asset for which there wasn’t a lot of details in their October 2023 announcement. I’ve been out of the game for a number of years but you know any deal was marketed, anyone had a chance to look at it, and ultimately KGT was the most interested (pronounced highest bidder). Their proposal with SilverBow, as a private going after a public, looks opportunistic and hand wave-y as they really haven’t had a chance to execute on these newly acquired assets they got at the highest price and now immediately want a premium for.

To quote Doomberg, let’s dig in.

Reserves. KGT has net debt of $246 mm. SilverBow has $1.221 billion of net debt. The “equity” as presented by Kimmeridge in their “follow up presentation” is irrelevant as it’s a balance sheet plug. So let’s look at the proved PV10 SMOG (yes!!!! It’s back!!). SilverBow SMOg is at $2.664 billion. KGT combined (including Blackbrush, presumably their 2023 purchase otherwise why break it out?) is $961 mm, of which BlackBrush is 61% but there isn’t a lot clearly public. Side note …. This from a June 2022 Reuters report

June 29, 2022 (Reuters) - BlackBrush Oil and Gas has placed some of its assets in south Texas for sale, seizing on a surge in energy prices, people familiar with the matter said on Wednesday.

The San Antonio, Texas-based company, in which Bain Capital Specialty Finance (BCSF.N), opens new tab is a major owner, has hired an investment bank to run an auction for more than 30,000 net acres (12,140 hectares) in the Eagle Ford shale formation, which produce around 11,800 barrels of oil equivalent per day. The baseline valuation of the asset's production would be around $430 million, although BlackBrush may seek a sale price in the "high hundreds of millions of dollars" to account for substantial undeveloped acreage in the area, the sources said.Currently, the company has 360,000 gross acres in the Eagle Ford, according to its website.

So, it checks out that this is a logical assumption that the deal failed, sold in October 2023 and they added some more acreage to make the numbers make sense.

NEW YORK and HOUSTON, Oct. 11, 2023/PRNewswire/ -- Kimmeridge, an investment firm focused on the energy sector, today announced that its affiliate, Kimmeridge Texas Gas ("KTG"), has signed a definitive agreement to acquire certain upstream assets from a private seller, as it expands its footprint in the Eagle Ford shale play. These assets, which include approximately 30,000 acres and current production of 65 mmcfe/d, have a strong degree of overlap with KTG's existing 75,000-acre position in the play, offering significant scale and operational synergies. KTG anticipates continuing its multi-rig program focused on the Eagle Ford and Austin Chalk, with a target of delivering over 500 mmcfe/d net on a pro forma basis in 2026.

SilverBow has a market cap of $873 mm which, including $1.21 billion of debt equates to an Enterprise Value or roughly $2.1 billion against reserves of $2.664 billion at $34 a share. At current levels, SilverBow is trading at a 35% discount to its PV10.

Meanwhile, KGT’s offer is to combine companies in exchange for $1.1 billion in stock (32.4 mm shares at $34/share plus the assumption of KGT debt. Their reserve value net of debt is $715 mm, equating to a 53% premium for the Kimmeridge assets. Kimmeridge will also put in $500 mm of new equity at $34 a share as part of the deal, but again, this appears to be at a 35% discount to PV10 for SilverBow while having crystallized a 53% premium for their own KGT asset (in math, get $1.1 billion for $715 mm, that’s $385 mm in premium which they are using $500 mm in new cash to buy a deeply relatively undervalued stock.)

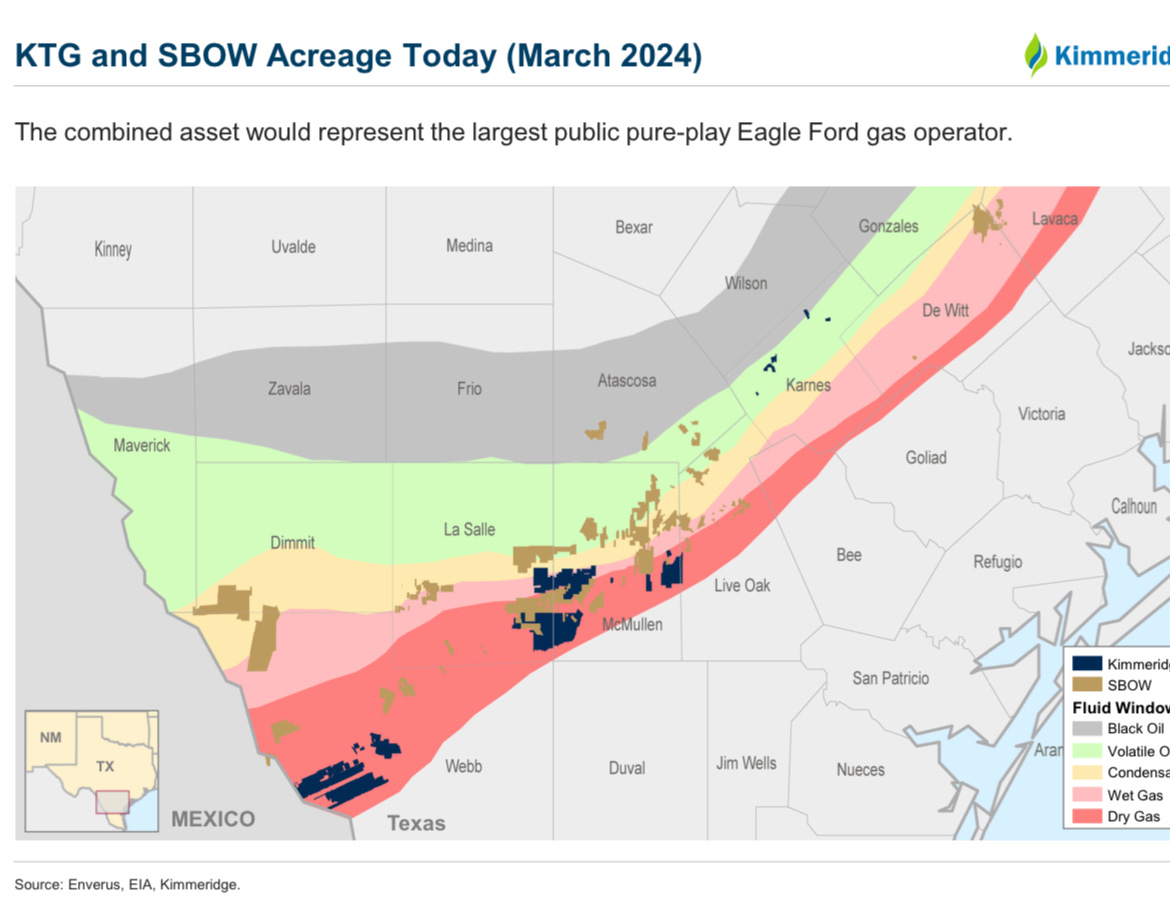

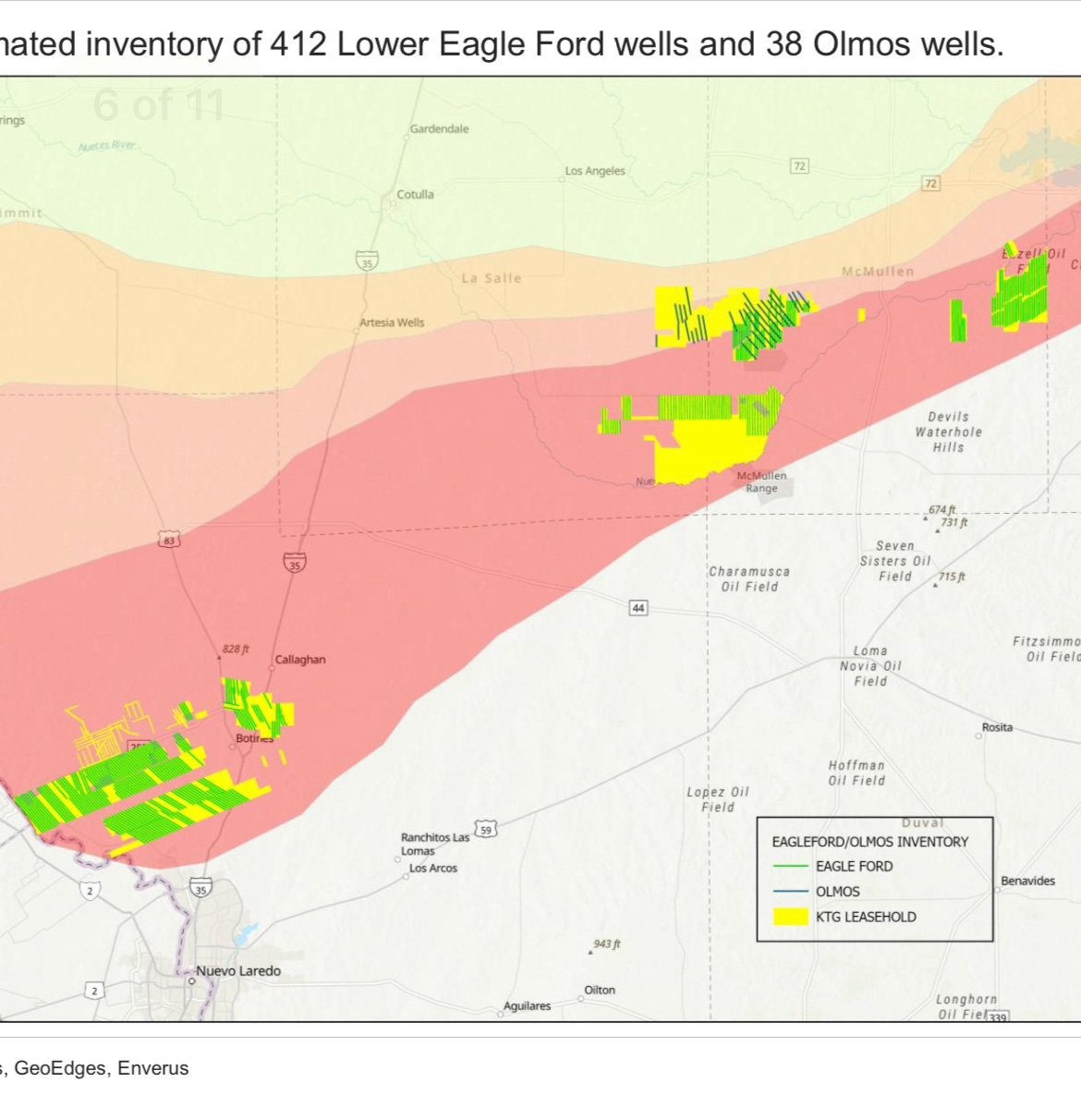

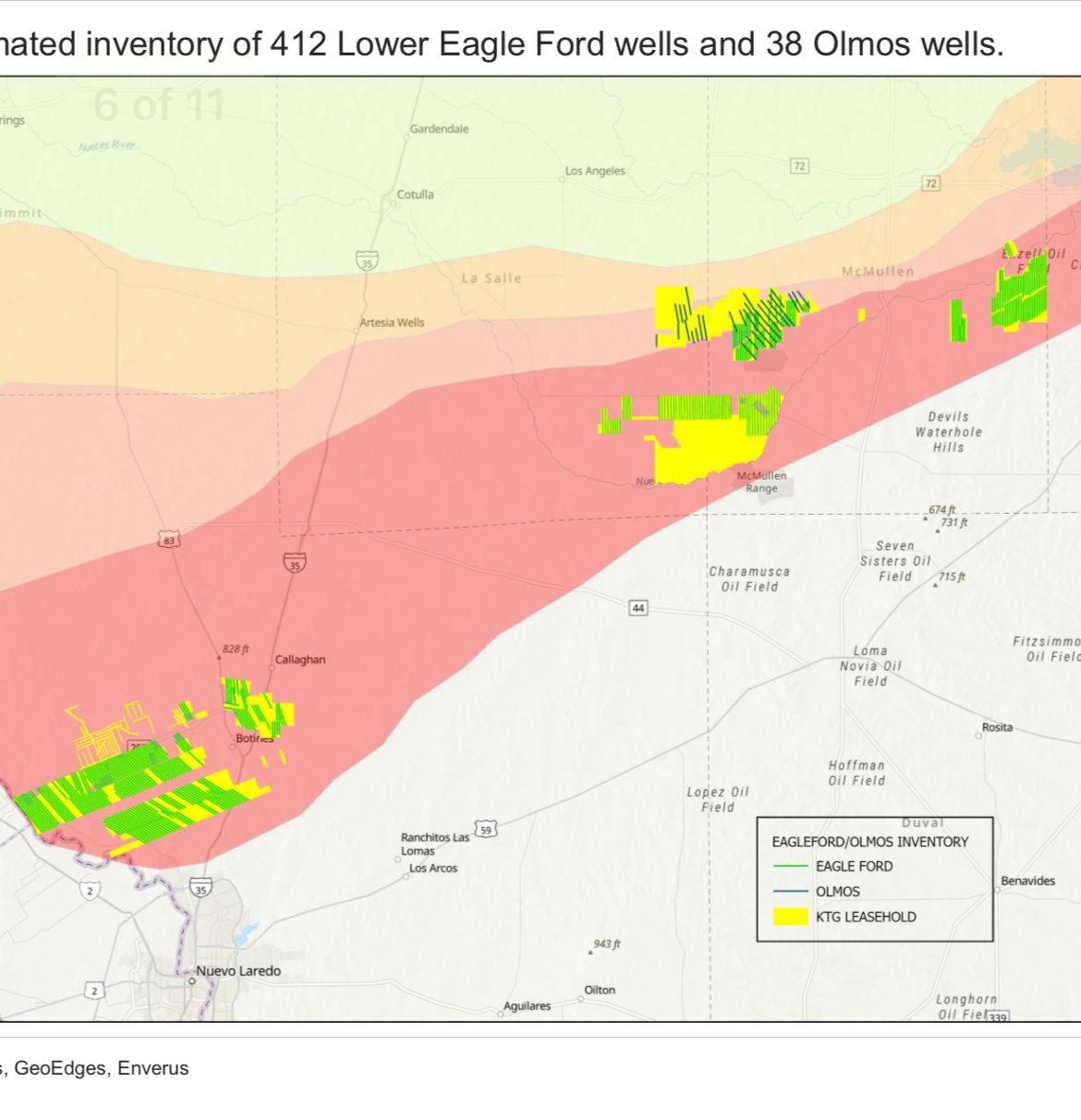

Here’s the Eagleford inventory.

No doubt you see what I see. Lots of well density. Not a ton of existing wells. Feels early. And at sub $2/mmbtu, what kind of rates of return do these get and how does it compete with SilverBow’s existing assets? As I said, Blackbrush was marketed, took more than a year to sell and everyone and their dog could have bud and KGT was the winner. Does this asset deserve a premium 6 months later?

I love Kimmeridge. I think they are brilliant and smart and I love this deal for them. But, to me, SilverBow is correct and were I on the board (which I’m not and I’m not holding my breath for any phone calls), I’d be exploring PubCo mergers with other companies that make more valuation sense.

But hey, what do I know? I’m just a lowly law student.

The Return of SMOG! Thanks for this analysis as I have a non-financial interest in this transaction.