EIA projects record oil production in 2023

EIA projects record oil production in 2023

I respectfully disagree. Here’s why.

According to the EIA, oil production in the US will average 12.41 mmbo/d in the US in 2023 and surpass the old 2019 record of 12.3 mmbo/d. In October of 2021, the EIA 914 report shows 11.5 mmbo/d of production, so 2023 will require 900 mbo/d of growth (~8%).

I disagree for three reasons.

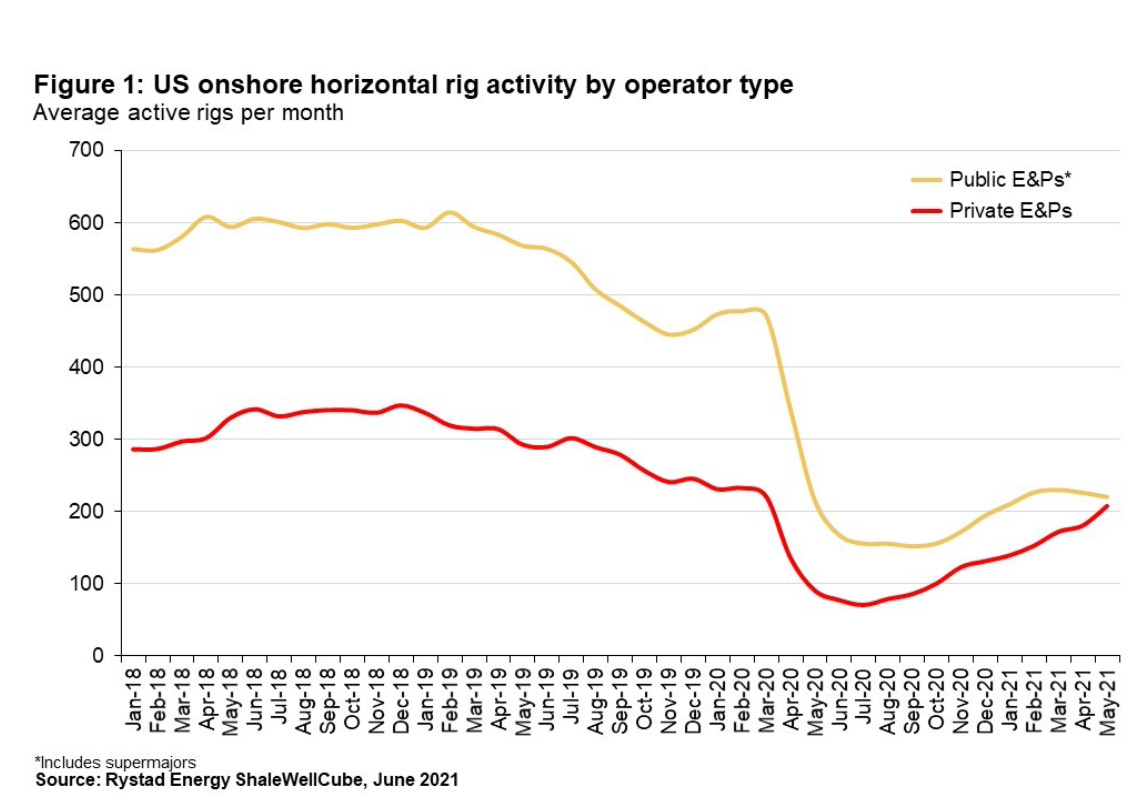

1. As you can see in the chart below, by mid 2021 (production coming on from that drilling now), private operators were running approximately half the horizontal rigs in the United States.

By and large, these companies can outspend cash flow (and are) to grow production to a level that makes them an attractive acquisition target at "accretive metrics." By accretive, a public buyer may trade at 6x cash flow, and they can buy said private company for 4x CF (ignoring peak production, short term declines and true NPV considerations for the moment). By allocating a 4x CF multiple to PDP (when flush production should be 2.5x), it masks the value allocation to the inventory and acreage costs. Felix did it with WPX. Double Point did it with Pioneer. And today, Tap Rock, Colgate, Birch, Ameredev, et al are all doing it now. The big IF is will there be enough tier 1 inventory left at the end of the drilling surge to sell the company or if buyers (as some CEOs I’ve talked to suggest) say they don’t want PDP at PV10 when their cost of capital is 9-12%. They need inventory at PV30, but no seller would sell at that price as long as they are confident they can drill it and hedge to lock in exceptional drilling economics today. But, the challenge with oil and gas, and why I am long term bullish price but bearish E&P company valuations, there is only so much inventory to drill. At some point, all companies have to transition to the blowdown case, at which point comes substantial declines. I think that happens before 2023.

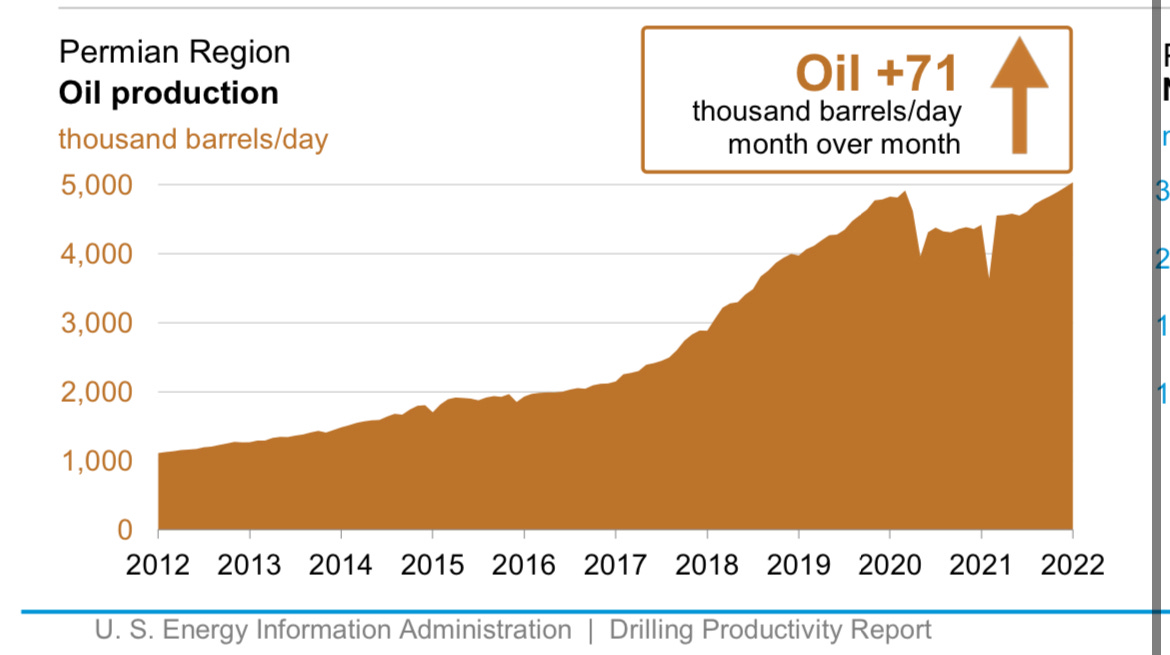

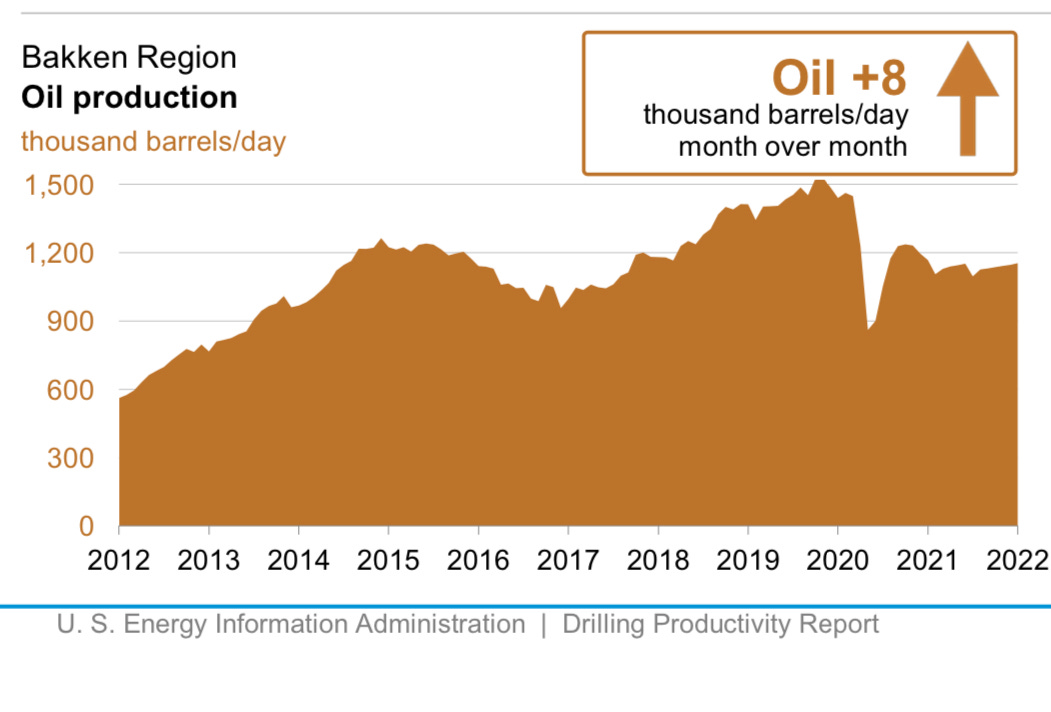

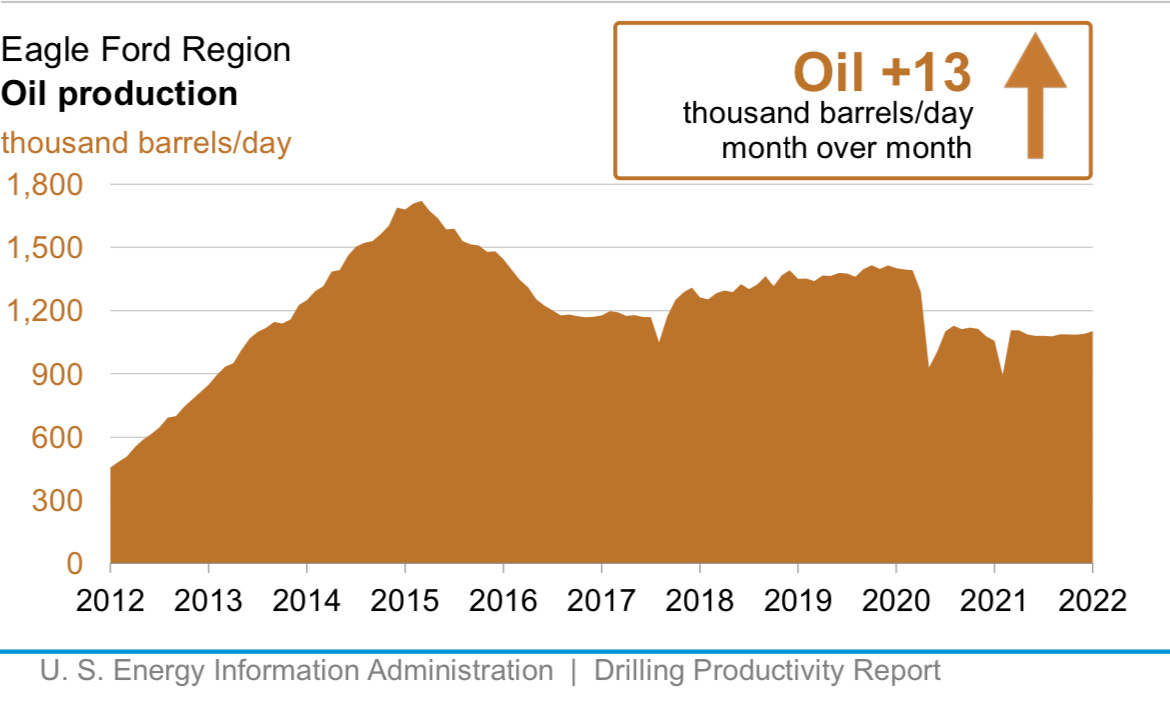

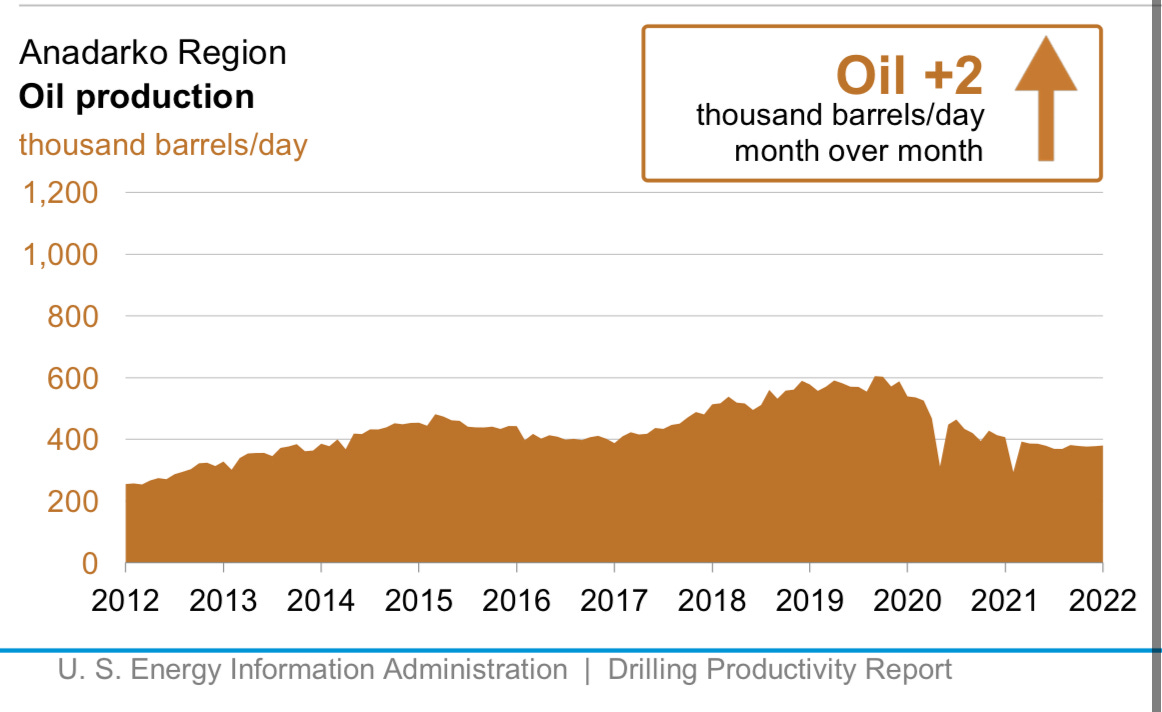

2. With 2 years of relatively low capital activity in basins like the Anadarko, Bakken and Eagleford, errors of spacing past are more clear than ever. Tight well spacing was always going to take 2-4 years to reduce the b factor from "1.3" to "1.0" and increase terminal declines from "6%" to "8%+". That, plus frac hits, lost reserves, and less access to capital to drill marginally economic “incrementally tight wells” in those basins will have operators focusing on maximizing EUR and ROR, rather than maximizing NPV by overdrilling (in my opinion). That limits the drillable inventory and growth in the non Permian basins. The Permian, as you can see in the chart below, has grown past 2019 highs. The rest of the basins, not even close. And yes, the Permian will continue to grow, but 20% in the next 12 months to meet the EIAs average 2023 number? I don’t think so.

3. In the same report the EIA projected a new oil production record in 2023 in the United States, they projected global demand for oil will reach 102.3 mmbo/d. What a turn of events from "the new normal" in 2020 that saw tele-commuting reduce demand and "we have reached peak oil demand." Fossil fuels aren't going anywhere, and EVs will not take over transportation for the foreseeable decades, as physics and supply chains limit their growth. HOWEVER, as interest rates rise, monetary stimulus in the system is reduced, and we see the actual economic damage that was done to the global economy from policy actions responding to COVID, I am less bullish on economic growth. Oil demand matches economic growth and the era of fed induced global growth is coming to an end, at least in the short term.

I think you're spot on - unless of course some hot new technology comes along and makes it possible to double or triple oil production from shale wells while cutting cost/bbl by 50%, cutting GHG emissions 50% and water production 75%.....

Can you narrow down your conclusions please. Is your position that 12.3 will be the peak annual US production rate? Or do you disagree with the timeliness of the forecast?