Credit Suisse teeters and the market is in real trouble

Credit Suisse teeters and the market is in real trouble

A guest post from Quoth the Raven

I am more comfortable being a bear and cynic. I don’t really trust people, I hate being surprised and hurt. And as such, 85% of the time I’m bearish. I have said for a long time I think the market is in for a major reckoning as a result of the policies implemented during COVID and that what will result is the love child of 2000 and 2008. I think we are close. Here’s a guest post that says it better than I could.

I was planning on publishing a different piece on something else this morning, but given the news over the last half hour I figured I would pen a quick note about the impending Credit Suisse mess.

For those that haven’t read, the distressed bank’s biggest shareholder, Saudi National Bank, which is 37% owned by the kingdom's sovereign wealth fund, has publicly ruled out further investment for the bank.

It’s the last message you want to send during a time where markets are already jittery following several bank runs and resultant bank shutdowns.

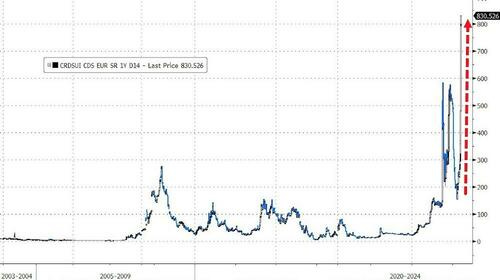

From an excellent Zero Hedge writeup of the situation so far this morning, this has led to “the cost of insuring the bank's bonds against default in the near term to distressed levels.”

"One-year credit default swaps for the embattled Swiss lender were indicated at 835.9 basis points on Tuesday's close of business, based on pricing source CMAQ. Other pricing sources point to a further rise on Wednesday, while a level of 1,000 would indicate serious concern," Bloomberg said.

Credit Suisse’s CEO was out defending the bank and its capital ratios today, but that doesn’t mean much in an investing environment where the smallest spark of bad news can immediately burst into a state-wide, California style wildfire. After the panic, it can almost become and afterthought that does more harm than good, or simply a headstone on the grave of the entity before it is even pronounced dead.

“I would ask everyone to stay calm and to support us just like we supported you during the challenging times,” Silicon Valley Bank’s CEO said just days before the bank was taken over by the FDIC.

“Signature Bank, a New York-based, full-service commercial bank, announced today updated financial figures as of March 8, 2023 and reiterated its strong, well-diversified financial position and limited digital-asset related deposit balances in the wake of industry developments,” Signature Bank wrote in a PR just 3 days before it was also taken over by regulators.

And now, today: "We have strong capital ratios, a strong balance sheet," said Credit Suisse Chairman Axel Lehmann.

Earlier this week, I wrote this piece where I lay out what I continue to buy and how my 2023 thesis continues to play out. While I’m not sure what’s going to play out over the short-term today in markets related to the Credit Suisse situation (the Dow has dropped about 500 points in the last hour alone), it’s a perfect example of what I have been saying the last few days, both on my blog and on my podcast. There’s been one big change over the last week.

Market psychology has broken

Despite yesterday’s rally - which astonishingly came in the face of Russia downing a U.S. drone over international waters - the broader point is that market psychology has changed significantly.

The only difference between these foregone conclusions last week and these foregone conclusions this week is that now market psychology has changed. People are likely to be slightly more risk adverse than they were weeks ago. And when you take “slightly more risk adverse” and multiply it by a hundred million market participants, the shockwaves and can be awe inspiring and result in even more risk aversion.

And that is what we are seeing now: people are scared of bank runs and investors - like the Saudi Bank - are going to be that much less likely to jump in and try and catch some of these falling knives. When bank failures and contagion are on the mind of investors, everyone starts pulling back their risk slightly. When the entire investing world does that collectively - with rates at 4% - well, look the fuck out below.

There’s a reason that I keep comparing sentiment to a snowball rolling down a hill: once it gets going, there’s no stopping it, and it only gets larger.

It’s also one of the reasons I continue to buy short dated index puts. You never know when you’re going to wake up one morning - not unlike today, though I’m not sure we’re going to see real fear just yet - and something has just…broken.

Now, the inevitable explaining away and digging into Credit Suisse’s counterparties is going to start. The Swiss bank isn’t necessarily direct contagion from Silicon Valley Bank, but that doesn’t mean there isn’t going to be contagion from Credit Suisse globally. You can bet dollars to donuts that depositors at the bank are drawing from their accounts at a rate that’s likely a bit higher than days past. And, with the Swiss National Bank refusing to comment so far today (it’s only 5 hours ahead in Geneva right now), I’m not sure the situation is going to resolve itself in time for the U.S. market to close today.

As Buffett would say, “Time to see who’s swimming naked”.

As I said on my podcast on Saturday, I’ve been saying for months that rate hikes take months, if not quarters, to make their way through the economic plumbing. I don’t doubt that the blowups were seeing now were probably put well into motion all the way back in mid-2022. Since then, rates have only risen and there has likely been a litany of other failures that have been put into motion that we don’t know about yet. As Forbes noted this weekend, the distress was already rearing its head at SVB by year-end 2022:

Only now does the rolling cycle of blowups continue on its merry way, with the detritus from 2022 likely to flush its way out of the system as we hit mid 2023. Additional stress and blowups are already foregone conclusions and will take place in areas of the market that the Fed isn’t bailing out just yet (and will likely surprise everyone when they happen - you’ll know these headlines when you see them).

We’re only just getting started.

With regard to positions I continue to keep and add, I’ll say what I said earlier this week. To some degree, the panicked banking sector is the beginning of why I have been positioning in gold and silver miners (GDX, SIL, PAAS, NEM, etc.) over the last year or two (in addition to the small fact that Saudi Arabia, China and Russia may openly challenge the U.S. dollar).

The geopolitical angle to my thesis for this year continues to also take ugly steps in the “right” direction with the most recent Russia/U.S. drone confrontation and nations like China, India and the Saudis all allying themselves further. I am happy owning and adding to the iShares U.S. Aerospace & Defense ETF (ITA), Raytheon Technologies Corporation (RTX) and General Dynamics Corporation (GD). I also own Lockheed-Martin (LMT) and Northrop Grumman Corporation (NOC), though they weren’t mentioned in my 2023 names.

With defense continues to come cybersecurity and I expect that iShares Cybersecurity and Tech ETF (IHAK), Palo Alto Networks (PANW) and CrowdStrike Holdings, Inc. (CRWD) will benefit from the Fed backstop and still have a fundamental case based on geopolitical volatility that continues to ramp up.

As I also reiterated on during a Palisades Gold Radio interview I did earlier this week (and will be published today or tomorrow), there is still no fear out there.

When there is, you’ll know it.