AirBnb Revisited

$106 billion market cap but limited appreciation for investors post IPO

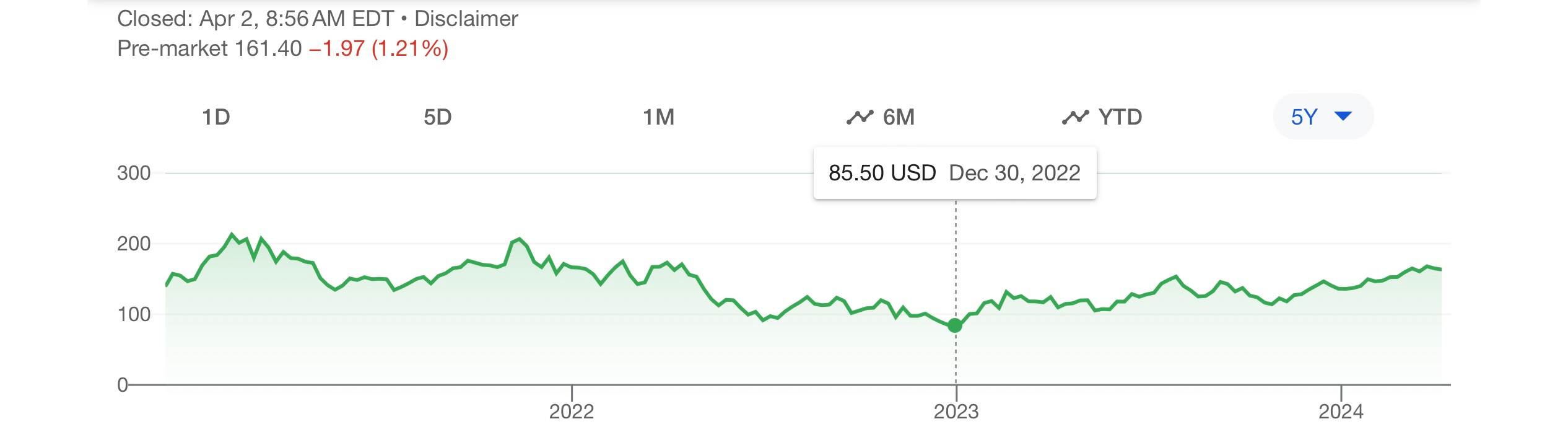

Just over 3 years ago, Airbnb went public and I wrote this about the company.

Once upon a time, there was this little thing called valuation. Airbnb is set to open today (Thursday, December 10) and the original indicated price was $68/share which would value the company at $47 billion. At the time of writing, the stock hadn't opened, and it was indicated at $150/share, which implies approximately a $103 billion valuation.

I like Hilton. It's a great hotel chain. Bill Ackman owns it and made it his poster child for the pandemic in March 2020 on CNBC. It‘s market cap is $30 billion. Its enterprise value is $40 billion…..

Today, Airbnb sits right around where the stock opened that day, at $164 a share and yielding a $106 BILLION market cap and having recovered 64% since the beginning of 2023.

Call me old. Call me obtuse. But for the life of me, I can’t figure out how this company is more valuable that EOG, or Oxy or even Hilton who possesses a market cap of $53 billion today ($62 billion enterprise value) which leases directly 51 properties, manages 800 others and franchised 6,679 properties to independent companies to minimize the physical assets it needs to own and pay for.

For Hilton, which boasts Trailing Twelve Month (TTM) revenue of $10.2 billion and net income of $1.141 billion, it trades at 5x revenue and 46x P/E. (excluding debt). I’m sorry … but what??? 46x!! If you want evidence that the public markets are totally F@&k’d and have become a casino, a 46x P/E ratio for a hotel brand will do it. Run the DCM on that at 10%…..

For Airbnb in 2023, the company reported revenue of $9.9 billion with earnings of $4.792 billion. In fairness, AirBnb has roughly the same revenue as Hilton and earn 4x the gross earnings which yields a 22x P/E ratio. But to me, more telling about their future prospects is that they have $10 billion of cash on the balance sheet and don’t have anything to spend it on other than buying back their stock (they do, to the tune of $2.25 billion last year).

How does Airbnb win? By using YOUR assets. From a business model standpoint, it’s pretty genius. They provide a technology platform which connects house owners with house renters and take a fee. In 2023, the gross booking value of houses was $73.3 billion over 7.7 million properties from 5 million hosts.

The question, as with Nvidia, is not “is this a good business?” It absolutely is. Look at the numbers! But the real question is “what is this business worth?” 80% of homeowners in the United States have interest rates lower than 5% and 60% have rates lower than 4%. That sure helps the inventory of homes AirBnb has access to. In 2021, there were 2.25 million active listings on Airbnb in the US alone and generate an average of $14,000 of revenue per year. So even against rising property taxes, increasing insurance costs, increasing electricity costs and inflation driving maintenance and service costs higher, the big bullet for Airbnb owners remains the mortgage, many of which are at interest rates dramatically below current rates of 7%.

Home prices are up 40% since Airbnb went public, on average. With leverage on the down payment, that’s a substantial gain for many homeowners, many of whom only own a second home for rental purposes. At what point does inflation, rising insurance and property tax costs on one’s primary house start to make the gain in the rental house look attractive enough to crystallize?

What if the housing market does, as I think it must, correct 40% to account for higher interest rates and lower affordability? What if the economy weakens and travel budgets for vacations are cut? What if the hotel lobby alongside angry neighbors (and let me tell you, I have angry neighbors at my place in Phoenix!) continues to be successful and massively restrict short term rentals which is where all the returns are made? 22x earnings against 18% year over year revenue growth and 150% net income growth might look impressive compared to 2022 coming off the pandemic. But how many new house owners are going to enter the fray as compared to those who want to take their chips off the table?

Realistically, Airbnb has a dominant position and as long as they scale their costs to reflect the number of bookings, the business will stick around for a long time. I love the platform and the rentals it generates in Arizona cover my fixed costs plus plus and make owning a second house for personal use 1-2 months a year very attractive. But would I want to own the stock at this valuation given the asymmetric risks to listings? Personally no. I’ve passively listed my house multiple times because it’s up so much since 2019. It wouldn’t take much for this host to be encouraged to sell it. How many other owners are in my boat on that one?

Time will tell, but it’s something I’m watching as a canary in the US economy coal mine….

Airbnb IPO

I will start by saying that until very recently, I loved Airbnb. I won't belabor the single unfortunate hosting experience and subsequent drama it created in my life for the last 75 days, but I wanted to put that out there. I don't own their stock, nor will I, and I'm unlikely to continue hosting through the platform. Throughout 2020, we have rented our…

I don’t disagree here. I don’t own either but o get your point fully on why Airbnb. They are leveraged to other assets so the largest risk is the rate at which they go away … if at all.

I do not disagree with the sentiment regarding ABNB.

Why shouldn't ABNB be worth more than HLT? They leverage other firm's assets and will churn out more cash flow over the next decade, no? ABNB can also grow top line revenue much easier than HLT. Both firms are clearly overvalued, but if you had to decide which one was more attractive to investors, wouldn't it be ABNB?