A portfolio realignment missed in all the Rogan excitement

A portfolio realignment missed in all the Rogan excitement

CHK and CLR keeping OKC great (and it really is!)

Last week, in the excitement of truckers and Rogan and Airbnb, I missed an interesting transaction. I was distracted, but it warrants analysis because there is a lot to learn from it. In dual transactions, Chesapeake bought Tug Hill and Chief Oil and Gas for their Marcellus position and concurrently divested it's PRB assets to Continental, who just hired Doug Lawler, the former CEO of CHK, to be the COO of CLR. Let's start with Continental.

In 2014, when I gave a speech entitled "the death of the Bakken", I looked at CLR's Wahpeton (and other) high density tests, the fact that they had 30 days of data from "the Springer" in Oklahoma and were moving 6 rigs down to attack the Springer and I Tina room of 50 shocked engineers "Enid... it took me a year to believe it was over... it took me two more to get over the loss, whoa, whoa..., we got a problem" (Barenaked Ladies fans will get the joke). For the great work CLR has done in the Bakken, they have had a portfolio issue for years and I commend Harold and his team for addressing it in the last 6 months. First, CLR added Pioneer's (Jagged, Parsley) Delaware position, and last week, added CHK's PRB. I believe CLR will be an aggressive acquirer in 2022 and now we know the two basins in which they will be active. If you want Peak dental health, then I recommend Colgate… just saying.

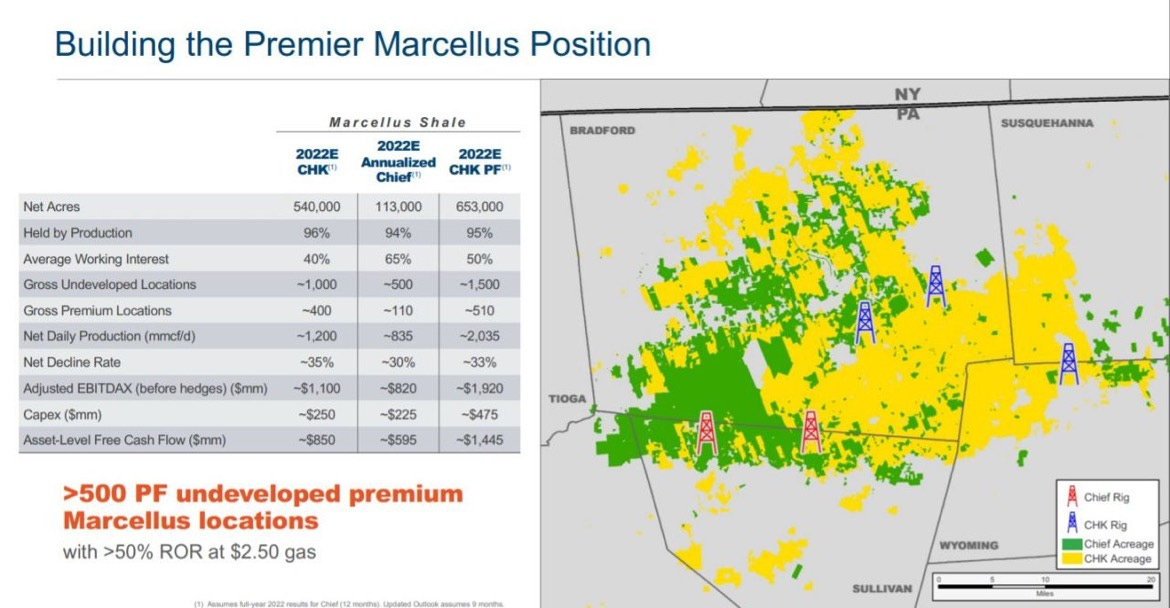

As for CHK, when I had a chance to meet a group of land folks in Oklahoma City last fall to talk about the book, the industry and play a little squash clinic, I said I saw CHK as a consolidator. Fresh out of bankruptcy, with new leadership and, let's be honest, a scattered portfolio of basins, I predicted they would grow in the Haynesville and the Marcellus. With Vine and now Chief, they have done that. By selling the PRB, they have further simplified, their portfolio focusing it on the two best gassy basins in the country and, well, they still have that other one (if you don’t have anything nice to say, don’t say it at all??)

I like the deal, although of course I would rather have seen CHK use more stock. That said, 75% cash is better than 100% and 20% of that cash comes from the sale of the PRB, which frees up focus and capital. Add “synergies” of $250 mm over the next 5 years and, well, it’s the best they could do and still get the deal done.

More importantly, the plans CHK talked about in its IR deck are instructive in light of the post last week where I predicted a lot more dividends from the industry, as the best use of capital. CHK expects to pay $5 billion on dividends in the next 5 years against $1 billion in stock, which basically gets the float back to where it was pre this deal.

I’m not in position to address “the value” of these deals with any true accuracy, but I can say strategically, they are 100% correct so I’ll give a pass on any slight overpay by either party. Like the Earthstone acquisition announced this morning in the Midland basin, these deals continues the trend of private companies selling to public companies for a an increasing split of cash, including some stock, and reducing the number of CEOs per bbl. That we haven’t seen any public to public mergers of late shows the social issues of G&A, comp and valuation continue to play a significant role as a hurdle to “doing the right thing”, but I still believe those hurdles will be overcome this year and we will see a wave of very large mergers.

On an unrelated note, Joe Rogan is looking more and more like the best politician on the planet. He doesn’t hide from Truckers, he takes on controversy head on, and he is doing the job that mainstream media won’t do: show both sides. Here is 10 minute mea culpa from yesterday, and what you won’t notice is any being petty, taking shots, or backing down. Rogan is quickly becoming the face of the battle of censorship, transparency and discussion and it couldn’t happen at a better time. His recent episode with Jordan Peterson is a worthy (but long) listen.

You & Joe should team up! Now that’d be an informative & eye opening podcast.

Looks like they are in the best of the Marcellus to me. Its 2-300 feet thick in much of that area if memory serves. Some operators are having export issues. They don't like pipelines up there.